.webp)

Embedded finance ecosystem: How the value chain works

After the first wave of platforms embed finance into their offerings, businesses across all industries are expanding value chains to attract and retain customers and tap into potentially huge pools of value.

How? Embedded finance increases access to financing for merchants and allows sustainable growth for both partners and their merchants. The result: it can drive growth, boost user engagement, increase loyalty, and add new revenue streams.

But how exactly does the value chain work?

What is the embedded finance value chain?

In the embedded finance value chain, there are several primary activities. These are the two main ones as they relate to managing capital:

- Inbound (the capital providers who provide capital at super low cost) - From an operational perspective, the platform used needs to ensure it can handle the capital and process all the API integrations. And from there, ensure the operation of the product happens automatically.

- Outbound - This ensures the partners get the funding, and it is sent off to the applicant.

Additionally, there are three key functions that allow for a more lucrative model that exceeds customer expectations. Here, we talk through how embedded finance providers can support the value chain:

- Marketing: Partners will be in charge with the embedded finance provider supporting here. The partner will often market on their platform and make it feel like their own product (this helps manage brand affinity and trust).

- Service: All services related to customer support can be handled by the embedded finance provider or the partner, depending on which will deliver the best experience for the customer. Remember, speed is key with embedded finance, so you need to be on it when responding to queries.

- Supporting activities: Embedded finance partners can also manage the strategic direction of the product to adapt to changing customer needs.

To put these key activities into perspective, let’s run through how the embedded finance value chain works in practice.

How the embedded finance value chain works in practice

Embedded finance is a modular technology architecture. We talk about it in four layers, relating directly to the people involved in the value chain - from capital providers to the SMEs receiving funding.

💰The Capital Provider

The first layer is the capital providers, this is essentially where the finance comes from. Our capital partners provide short duration, self-liquidating SME products.

⚙The Financial Product Provider

The next layer is the platform layer. This is the embedded finance platform, which is usually provided as a white-labelled solution. Like YouLend.

🔗The ‘embedder’

Next we have the partners layer - these essentially ‘embed’ the solution within their own platforms. These businesses and brands need to meet customer needs in a more integrated way to build more loyal and long-term relationships. Brands also win by expanding their portfolio and, in the end, gain more satisfied clients.

Moreover, all this comes at a low price and fast pace, thanks to the embedded finance model.

👩💼👨💼The end customer/merchant

And the final layer is the SME looking for finance (more on this in our new guide). Customers are increasingly becoming more empowered, demanding integrated experiences with the services and products they already use. In fact, according to McKinsey research, users are flocking to these multi-product customer experiences, also known as ecosystems.

To sum up, the four main players involved in embedded finance are:

- 💰 Capital providers: Companies which possess funds and/or banking licences and open their API to partners and providers.

- ⚙ Fintech/third party provider: The technological company which acts as a bridge between the capital providers and the business embedding finance.

- 🔗 Embedder: The business or brand interested in offering financial products to its customers.

- 👨💼 Customer: In this case, this is the SME that needs access to finance.

With this approach, all parties have the chance to either improve their existing offerings and/or grow their businesses.

The importance of APIs within the value chain

How do these different players function together as an ecosystem to deliver value for everyone involved? The answer is APIs.

eBay is a perfect example. By offering embedded finance products via APIs, it can now offer merchants a unique one-stop-shop to manage their cashflow and sell their products. eBay already has a vast database of merchants in constant need of tailored financing sources, so expanding their user experience with.

From a technology point of view, an embedded finance partner should provide API integrations which enable the embedded finance offering to feel like it's part of a merchant's own ecosystem.

That’s because fundamentally, strong API integration creates a better user journey for the merchant. And it makes it easier to create customised and automated workflows - with shared data to create instant funding.

💡Top tip: We recommend you look for a partner that is collaborative and 100% acquirer agnostic. This ensures designs are created to make sure merchants feel they are in a comfortable environment.

Benefits of outsourcing embedded finance

Building an embedded finance solution takes time and specialist skills. Even for businesses already in the financial industry, bringing an embedded finance solution to market is tricky. That’s why many businesses turn to outsourcing to a specialist.

With the right embedded finance partner, you can tackle regulatory requirements, protect reputation and satisfy customer needs.

Here’s how:

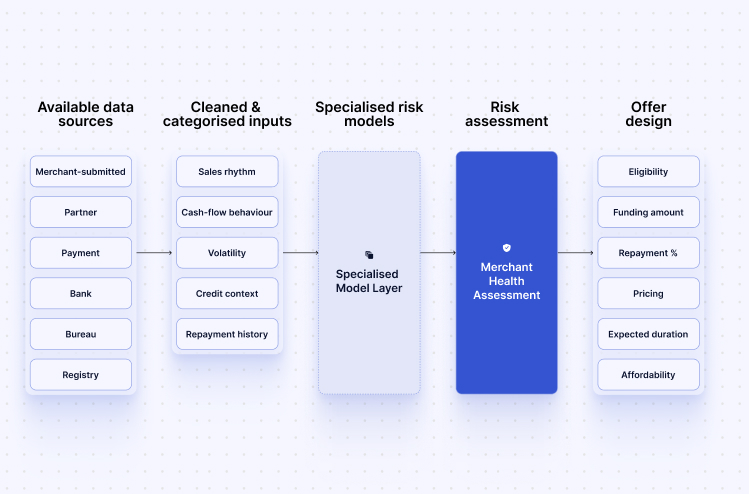

>> New and more accurate risk assessments - Because embedded finance providers leverage data beyond what traditional financial institutions look at, they can offer more competitive funding offers. This includes both publicly available data, such as social media presence or website traffic, and internal data provided by you, the company that wants to embed financial products.

>> Additional source of enhanced information - As well as payment behaviour, you can leverage non-credit payment behaviour insight, such as total traffic and engagement data, which can help better estimate future revenue and default risk.

>> Improved customer satisfaction - Instant processing of credit applications is a smooth and satisfying experience for business owners - which can promote higher loyalty with merchants.

How embedded finance benefits the entire value chain

- For merchants:

Access to live payment data

Instant liquidity/payouts

Faster, more flexible, higher acceptance rate, more affordable

- For finance providers:

Partners - increase loyalty/high partner retention (20-25% LTV)

Merchants - 36% increase in core sales

For capital providers - Acquire more merchants

Final thoughts: Why embedded finance is so important in today's value chain

To meet the rising demand for embedded finance, financial institutions, marketplaces, and PSPs are increasingly moving towards it. That’s because end-users love the convenience and simplicity that embedded finance brings to their lives, and it seems this trend is only going to continue.

What’s more, technology advancements will continue to transform and enhance embedded finance, expanding the financial services ecosystem and enriching the customer experience along the way. And running in parallel, regulatory changes such as open banking will encourage collaboration between banks, fintechs, and other third parties to increase competition and facilitate collaboration.

Final word. Embedded finance is altering the lending landscape. They provide new revenue streams, new types of competition and a new era of partnerships. For example, with companies like YouLend it saves hiring entire teams of finance, IT and product developers to support the new offering.

The need for embedded finance is only going to rise. And if you choose to outsource, make sure you choose a partner that supports development - with the ability to manage open APIs and technological changes.

.png)

.png)

%20(1).jpg)