.webp)

Traditional Credit Access Problems for SMEs

There are about 6M SMEs in the UK, accounting for 99% of all businesses and 61% of employment. The average 5-year survival rate of SMEs, pre-pandemic, was 42.5%. Approximately 29% of new businesses close down due to a lack of cash or funding. As discussed in our recent post the number of new businesses incorporated has accelerated as we emerge from COVID-19 lock-downs. With 390K businesses born each year, as many as 100k new businesses shut down every year due to lack of funding.

There is a significant demand for credit amongst SMEs. The British Business Bank said 45% of SMEs applied for external funding support in 2020 compared to 13% in 2019. The growth of SMEs in the UK market has far outpaced the growth of larger businesses, yet gross lending flows to SMEs by banks have remained flat over the past decade. Availability of credit for SMEs is clearly a major issue for their own health and the broader economy. Traditional sources of credit model a strong dependence on the proprietor’s credit history but these models leave out an ‘invisible’ population:

- Younger people with a limited established credit record

- Older people who may have paid off their mortgage or not relied on credit products

- Unbanked who are often credit invisible

- Recent immigrants with no credit footprint

A study from Experian estimates there are 5.8M adults in the UK with such a ‘thin’ or non-existent credit file, meaning they will have limited or no access to formal credit options.

Opportunity for Alternative Lenders

Consumers with thin or non-existent credit files provide an opportunity for lenders to use alternative data to make credit decisions. Access to enhanced information (alternative data) would also increase available funding options to those marginally declined - people narrowly rejected for a credit card or personal loan, but who are unlikely to default. Experian estimates this group represents a further 2.5M ‘thick-file’ customers.

‘Alternative’ data refers broadly to any information that has not historically been part of credit reports. Examples include non-credit payment behaviours of customers, as well as metrics around the perception of the SMEs amongst their customer bases.

The biggest consumer reporting agencies have realised the importance of non-credit payments in assessing the full profile of customers. Experian have started advertising their ‘Boost’ service that allows customers to share repayment history for expenses, like utilities and monthly council tax bills, in order to boost credit bureau scores. In the US, FICO has introduced 'FICO Score XD' in partnership with LexisNexis Risk Solutions and Equifax to serve the credit-invisible consumers by including utility, phone, and TV bill payment data in their reports. Currently, traditional credit bureaus could only see if someone had unpaid utility or phone bills that have been turned over to collections agencies. But with consumer-permissioned data, a consumer could permit financing providers to access their record of paying bills on time. Instead of only being penalized for missed payments, a consumer could get rewarded for on-time payments.

Instead of only being penalized for missed payments, a consumer could get rewarded for on-time payments.

This shift indicates that the industry has crossed the bridge to include the ‘invisible’ population in the traditional credit market. However alternative data can go above and beyond mere payment histories.

Alternative data leveraged by YouLend

YouLend uses credit risk modeling and alternative data sources to improve underwriting speed, accuracy, and outcome. Our credit risk system is rooted in sourcing unpolluted, non-correlated quantitative inputs rather than subjective human inputs, which in our opinion is slow and distorts the value of model output.

SMEs, in our opinion, are a distinct kind of client with unique needs that require non-traditional risk-management tools and methodologies developed specifically for them. By relying exclusively on credit reports and traditional risk modeling techniques, many financing providers ignore some of the best risk predictors in an increasingly digital world of SMEs. Credit bureau scores can be good predictors of financing repayment but should only be one of several parameters in a predictive model. The problem is most pronounced in the case of SMEs with shorter credit histories or high growth rendering their earlier credit history less relevant.

By relying exclusively on credit reports and traditional risk modeling techniques, many financing providers ignore some of the best risk predictors in an increasingly digital world of SMEs.

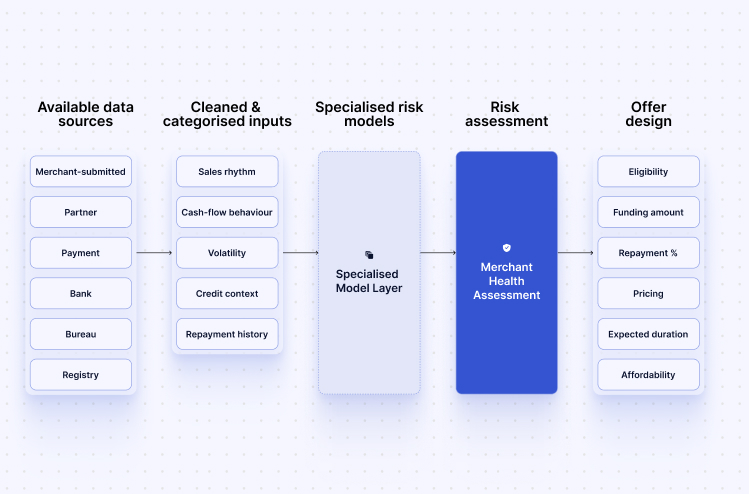

At YouLend, we have compelling evidence that partner-sourced transaction-level information coupled with cash flow variables, not conventionally used in risk scorecards, are the strongest predictors of credit risk across different target segments. The transaction-level information, sourced from our commercial partners, allows the algorithms to generate deeper insights into the customer behaviors of our applicant base. We are able to identify customer concentration risks, average transaction sizes, repeat customer purchase behaviors at the merchant site that serve as powerful predictors informing of the creditworthiness of the business. Hence, we are not assessing merely the probability of a merchant not repaying YouLend, we in essence are assessing the risk of a merchant losing their customer base that drives those repayments. These observations are backed by a study conducted by FinRegLab in the US. Their study, relying on data sourced from six alternative consumer and small business lenders, reported that cash flow variables were highly predictive of credit risk across the diverse set of companies, populations, and products.

Incorporating cash flow-based variables into the risk models allowed YouLend’s algorithm to successfully navigate complex region-wise lockdown measures introduced due to the pandemic. By following the cash flow (the heartbeat) of the business, YouLend’s algorithms automatically adjusted the creditworthiness of the business to the new normal. Our algorithm utilizes traditional inputs like credit bureau reports and management accounts (where available). But a significant lift is introduced in default prediction by including the above-mentioned cash flow-based variables, the strength of social media presence of businesses, digital footprint of the business, and other uncorrelated data into the risk algorithms.

By complementing (and not replacing) traditional underwriting parameters with others that are correlated with affordability and propensity to repay financing, YouLend’s approach understands and quantifies risk associated with all SMEs: those with a credit history and those without it; as well as those with a brick-and-mortar presence, and those with only an online presence. These alternative data sources enable YouLend to provide funding to businesses previously excluded from the finance market. These might be asset-light businesses, where the data become the new “collateral”, or businesses with minimal trading history. YouLend at the moment provides funding to businesses with as little trading history as three months.

In the 4 years since launch, YouLend’s model of incorporating alternative data has demonstrated solid performance and has continuously improved with additional predictors and information. The model has been successfully stress-tested through COVID-19 and multiple lockdown measures. We continue to stay on track to create a model that scores traditional and alternative data equitably to expand financial inclusion.

.png)

.png)

%20(1).jpg)